IOSCO Tokenisation warning for RWA markets

IOSCO‘s tokenisation warning lands at exactly the wrong moment for anyone selling tokenisation as a free, clean structural upgrade. In its Final Report on Financial Asset Tokenization, published on Tuesday, IOSCO acknowledges the…

IOSCO‘s tokenisation warning lands at exactly the wrong moment for anyone selling tokenisation as a free, clean structural upgrade. In its Final Report on Financial Asset Tokenization, published on Tuesday, IOSCO acknowledges the efficiency gains but makes the core point plain: the technology does not delete risk. It redistributes and amplifies it, especially where legal claims, operational resilience and retail access are poorly designed.

What the IOSCO tokenisation warning says

This is IOSCO’s first detailed, global sweep of real-world tokenisation: pilots in tokenised money market funds, fixed income, and institutional platforms rather than pitch decks. It sits alongside its 2023 crypto and DeFi recommendations and applies the same test: same activities, same risks, same regulatory outcomes.

The message is not anti-tokenisation. It is a calibration:

- Tokenisation can shorten settlement cycles, improve collateral mobility and enhance transparency.

- But without legal certainty, credible settlement assets, interoperable infrastructure and robust governance, those same features can magnify familiar failures.

In other words, calling it “on-chain” does not earn lighter treatment. It invites closer scrutiny.

IOSCO’s Final Report on Financial Asset Tokenization

IOSCO’s Final Report on Financial Asset Tokenization

The upside is real, but conditional

IOSCO recognises that putting traditional assets on distributed ledgers can make markets cleaner and faster:

- Near real-time settlement cuts counterparty and operational risk.

- Immutable records support more reliable ownership and transfer histories.

- Fractionalisation and programmability can unlock new funding and collateral models.

However, the report quietly undercuts the more breathless narratives: adoption is still limited, many pilots lean on legacy rails, and a credible settlement asset layer is missing or experimental. Tokenisation’s promise survives, but only as part of a hybrid market structure, not a wholesale overnight replacement.

Legal ownership and the risk of “paper-thin” claims

The sharpest concern is legal.

If an investor holds a token that represents a bond, unit or deposit, when something breaks, what do they actually own? The underlying asset, a claim on an intermediary, or nothing that stands up in court?

IOSCO highlights:

- Divergent national laws on what constitutes definitive title

- Complex chains of intermediaries and wrappers

- The risk that, in insolvency, token holders discover they sit behind other creditors

For regulators and serious institutions, this is the red flag. Until legal finality is aligned with the tech stack, tokenisation risk is not exotic; it is just harder to untangle at speed.

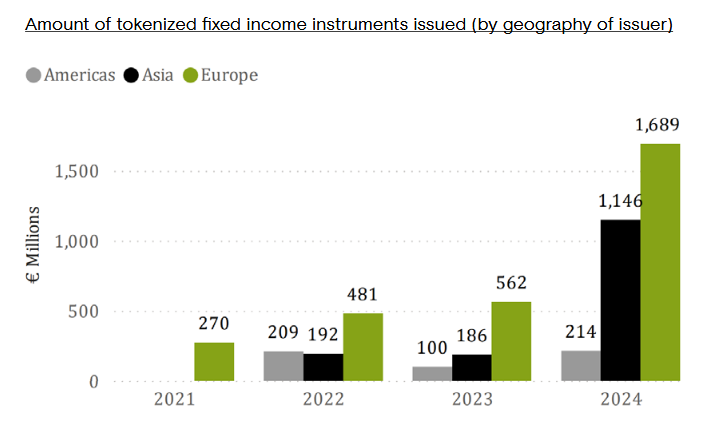

Source: AFME’s DLT-Based Capital Market Report 2024

Source: AFME’s DLT-Based Capital Market Report 2024

Operational fragility behind the glossy interfaces

The report then turns the usual “code is law” pitch on its head.

Smart contract bugs, failed upgrades, validator outages, key loss, oracle failures and bridge dependencies translate directly into frozen assets, failed settlements, or distorted NAVs for tokenised funds. Cross-chain experiments compound the blast radius.

IOSCO’s point is blunt: resilience standards that apply to central securities depositories and systemically important infrastructure do not get softer because the stack is on Ethereum or a permissioned variant. For system-relevant tokenisation, the bar goes up, not sideways.

Market structure, intermediaries and quiet shadow banking

Tokenisation does not remove intermediaries; it rearranges them.

New actors sit between investors and assets: tokenisation vehicles, platform operators, custodians, oracle providers, node operators. Some are regulated; many are not. Their failure modes look a lot like shadow banking: maturity and liquidity mismatches, opaque risk transfer, and correlated exposures.

IOSCO warns that without consistent oversight, regimes will fragment and regulatory arbitrage will thrive. That is an invitation for coordinated enforcement, not a gap to be marketed.

Retail investors: first in, last protected

The IOSCO tokenisation warning is especially clear on the retail angle.

Open, 24/7, global platforms plus tokenised exposures to complex instruments create the classic trap: products that look simple, trade like coins, and behave like leveraged credit or rate bets under stress.

Key concerns:

- Mis-selling of tokenised products framed as “safe yield”

- Thin liquidity and stale pricing in stressed conditions

- Over-reliance on platforms with weak safeguards or poor disclosure

The direction of travel is obvious: expect IOSCO members to extend suitability, disclosure, governance and marketing rules directly into tokenised offerings, not carve them out.

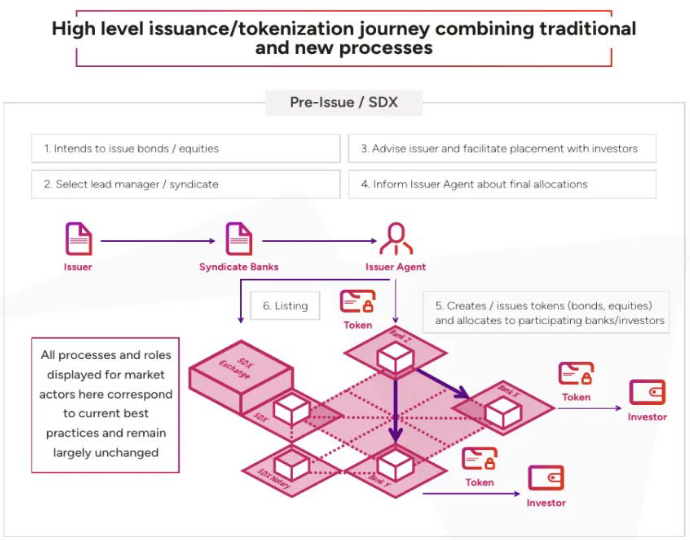

The issuance process of the UBS bond on SDX.

The issuance process of the UBS bond on SDX.

What regulators and markets should do next

IOSCO’s recommendations are evolutionary rather than theatrical:

- Apply existing securities and market integrity rules to tokenised assets with discipline.

- Map tokenisation pilots against crypto and DeFi policy recommendations; close the gaps.

- Demand legal clarity on ownership, custody, and insolvency outcomes before scale.

- Treat critical tokenisation infrastructure like other systemically important market utilities.

For credible issuers and institutions, this is not bad news. It is a blueprint: build products that can survive IOSCO’s checklist and you inherit regulatory legitimacy as an asset, not a tax.

The signal beneath the hype

Strip away the headlines and the warning does two things.

It validates tokenisation as a serious, monitored development in global markets; this is no longer a side-show. And it sets the expectation that any meaningful deployment will live inside full-strength regulatory architecture, not on the edges of it.

For anyone building tokenised funds, bonds, or collateral platforms, the trade-off is now explicit: you can have scale and credibility, or you can have shortcuts. Not both.

Disclosure: This article is for information purposes only and does not constitute investment advice, legal advice, or an offer of any financial instrument.

From the YFarmX archive · originally published on the previous site