The Bank of England stablecoin consultation

The Bank of England stablecoin consultation published on Monday does something rare in crypto policy: it stops hand-waving and lays out a concrete operating model for sterling stablecoins that want to sit inside the UK’s monetary system…

The Bank of England stablecoin consultation published on Monday does something rare in crypto policy: it stops hand-waving and lays out a concrete operating model for sterling stablecoins that want to sit inside the UK’s monetary system rather than on its fringes. The proposals turn “systemic” sterling stablecoins (those used widely for payments) into tightly regulated payment infrastructure, jointly overseen with the FCA and shaped with HM Treasury, rather than speculative offshore instruments.

Who This Regime Targets

The consultation focuses on sterling-denominated stablecoins issued by non-banks that could become integral to everyday or corporate payments in the UK. HM Treasury will formally designate which arrangements are “systemic”, but the logic is straightforward: if disruption to your coin could damage financial stability or undermine confidence in sterling, you are in scope. The assessment looks at how widely people and firms use the coin for real-world payments, how easily users can switch away, and how deeply the system connects into banks and market infrastructure.

That judgment-based approach is intentional. It lets authorities treat, for example, a big-tech-issued sterling stablecoin integrated into e-commerce and social platforms as systemic from day one, while avoiding automatic over-regulation of tokens whose main use remains trading on crypto venues. It sets a clear expectation for serious entrants: if you plan to be “the” GBP payment coin, expect Bank of England scrutiny from launch.

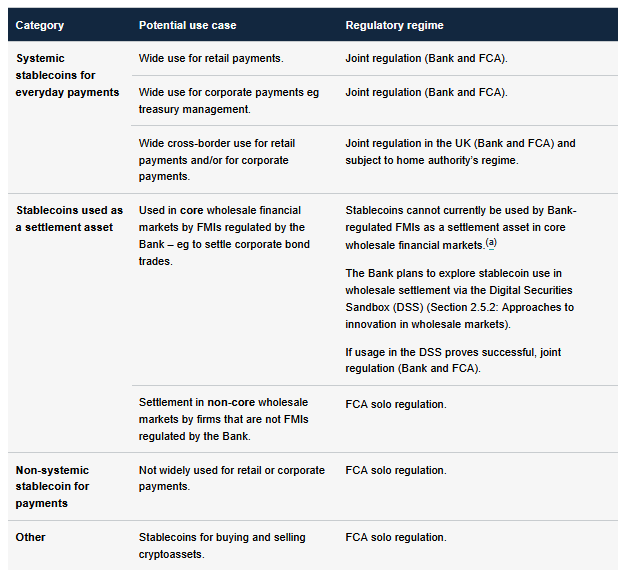

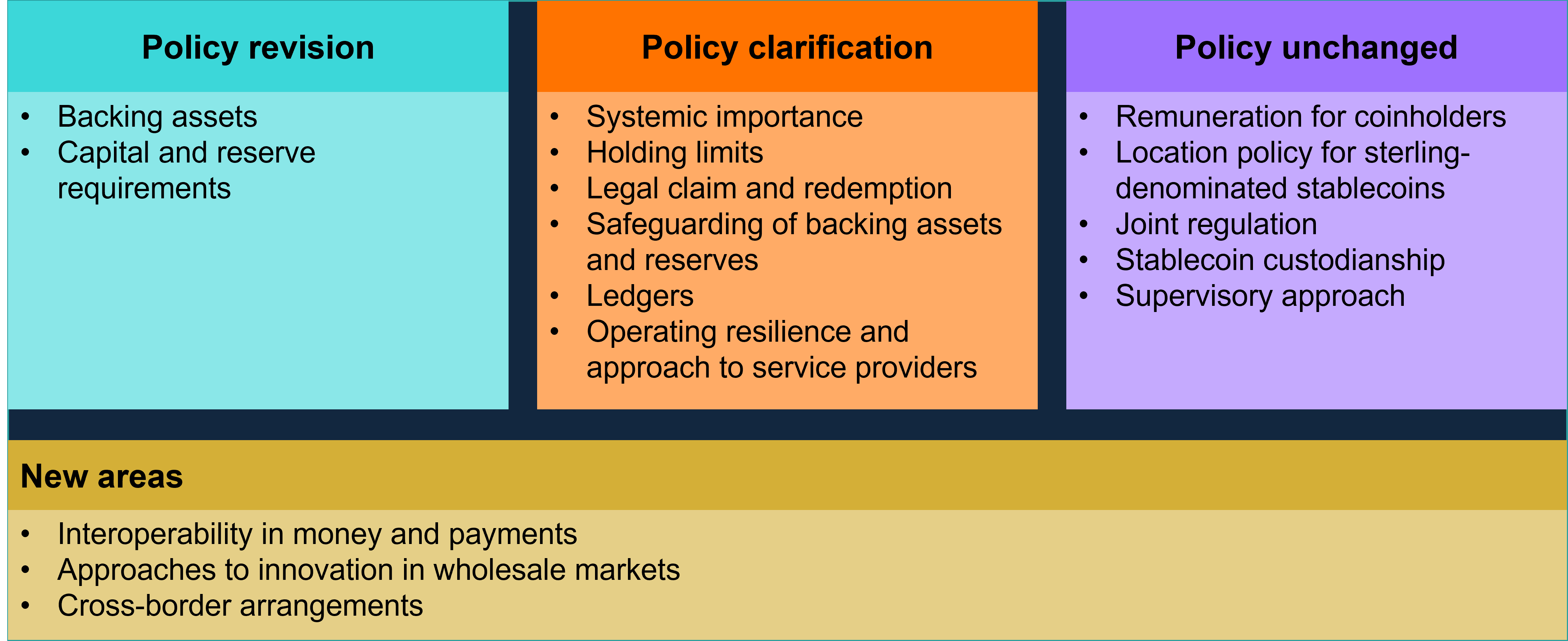

Overview of how sterling-denominated stablecoins issued in the UK would be regulated. https://www.bankofengland.co.uk

Overview of how sterling-denominated stablecoins issued in the UK would be regulated. https://www.bankofengland.co.uk

Backing, Capital and Legal Structure

Once systemic, a sterling stablecoin must look far more like critical market infrastructure than a yield farm with a logo.

The Bank proposes a conservative reserve model anchored in the UK. A significant share of backing must sit as unremunerated deposits at the Bank of England, giving issuers immediate liquidity and anchoring one-for-one redemption at par; the rest may be held only in short-term sterling UK government debt, providing limited income without exposing users to credit or duration games. Temporary deviations are allowed to handle large redemptions, and the Bank is considering a restricted liquidity backstop for solvent issuers. Together, these measures aim to make systemic stablecoins dull in the best possible sense: boring reserves, predictable behaviour.

On top of that, issuers must hold real capital and dedicated reserves. The Bank expects enough high-quality capital to absorb major operational and business losses, plus ring-fenced liquid assets held on statutory trust to cover movements in backing asset values and to fund an orderly wind-down. Crucially, coinholders gain a direct beneficial interest in these safeguarded pools, not a vague unsecured claim if the issuer fails.

For builders, this shuts the door on using client funds as a risk-on treasury strategy. If you want systemic scale in sterling, you raise equity and run a clean balance sheet.

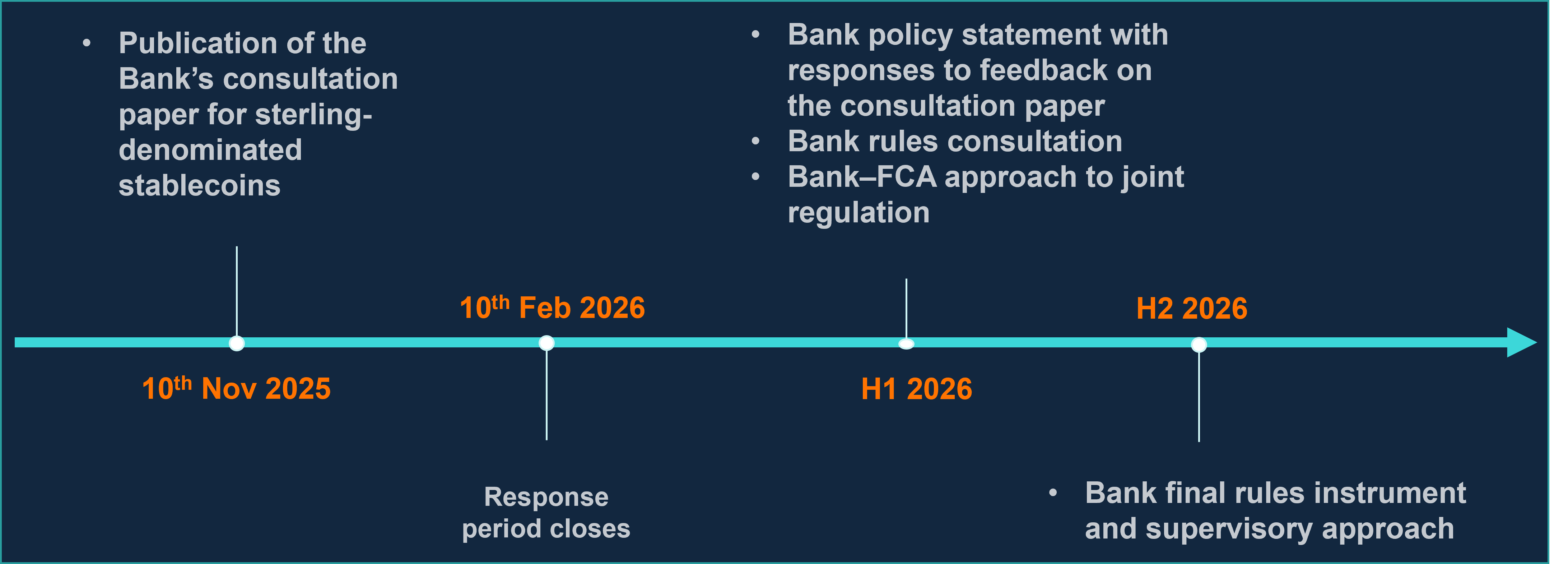

The consultation will remain open for feedback until 10 February 2026, after which the Bank of England aims to finalise the framework in the latter half of the year.

The consultation will remain open for feedback until 10 February 2026, after which the Bank of England aims to finalise the framework in the latter half of the year.

Legal rights and redemption mechanics lock in the “money, not token” status. Every holder must have a clear legal claim on the issuer and the ability to redeem at par in fiat within tight timeframes, with any fees transparent and proportionate rather than disguised haircuts. Using intermediaries for redemption is fine, but the issuer remains on the hook. The architecture has to support reliable, same-day exit into pounds under normal and stressed conditions.

Managing Systemic Risk

The consultation squarely addresses the political fear: a frictionless exit from bank deposits into “safer” stablecoins during stress. Drawing on its parallel Financial Stability Paper, the Bank signals transitional per-coin holding limits for individuals and businesses as a circuit breaker while the system adjusts. The aim is not to cap digital money forever, but to prevent a sudden, automated drain of deposits that could destabilise credit provision before banks and markets adapt. The Bank is explicit that it intends to relax and remove such limits once risks are better understood and managed.

Jurisdictionally, the message is uncompromising. Any non-UK group issuing a systemic sterling stablecoin into the UK must operate through a UK subsidiary, hold backing assets and capital in the UK, and sit directly within the domestic supervisory perimeter. For large non-sterling stablecoins with systemic UK usage, the Bank leans toward deference to credible home regulators, but only where their regimes and cooperation arrangements deliver comparable outcomes; otherwise, it reserves the right to act.

Overview of the Bank’s proposed policy approach compared to the 2023 discussion paper.

Overview of the Bank’s proposed policy approach compared to the 2023 discussion paper.

On technology, the Bank does not ban public permissionless blockchains, which matters for builders. Instead, it makes issuers responsible for ensuring that their chosen ledger setup delivers clear accountability, robust settlement finality and strong operational resilience, including cyber defences, to standards equivalent to traditional systemic payment systems. Permissionless chains remain in play, but “no one is in charge” is not acceptable once your token is functioning as systemic money.

A Multi-Money Future. Why This Consultation Matters

The consultation sits within a broader strategy: a UK payments ecosystem where commercial bank money, tokenised deposits, systemic stablecoins and a potential digital pound coexist and interoperate. It connects directly to the Digital Securities Sandbox, new RTGS synchronisation work and the Retail Payments Infrastructure Board’s mandate to design next-generation rails that support programmable, interoperable value.

For serious projects, the signal is clear. The UK is not trying to ban stablecoins; it is inviting them into the core of the financial system on disciplined terms. If you want to issue or integrate a sterling stablecoin that people use for salaries, shopping or wholesale settlement, you must accept central-bank-level transparency on reserves, UK law on safeguarding, enforceable redemption promises and infrastructure-grade resilience. In return, you gain regulatory clarity and a path to plug into the heart of one of the world’s major financial centres.

Theconsultation will remain open for feedback until 10 February 2026, after which the Bank of England aims to finalise the framework in the latter half of the year.

Disclaimer: This article is for informational and educational purposes only and does not constitute legal, regulatory or investment advice. Always seek qualified professional advice before acting on regulatory proposals.

From the YFarmX archive · originally published on the previous site