How CARF turns UK crypto exchanges into tax reporting hubs

From 1 January 2026, the UK will plug its crypto industry into CARF, the OECD’s Crypto-Asset Reporting Framework. Reporting cryptoasset service providers (exchanges, brokers and certain wallet platforms) will have to identify their…

From 1 January 2026, the UK will plug its crypto industry into CARF, the OECD’s Crypto-Asset Reporting Framework. Reporting cryptoasset service providers (exchanges, brokers and certain wallet platforms) will have to identify their users, aggregate their transactions and send structured data to HMRC, which will then share information with other CARF countries and run domestic compliance checks.

From OECD standard to UK law: what CARF actually does

CARF was designed to close a gap in the Common Reporting Standard (CRS), which covers bank and brokerage accounts but not most crypto activity. Under the UK implementation, CARF requires reporting cryptoasset service providers (RCASPs) to register with HMRC, carry out due diligence on their customers and report tax-relevant information on in-scope transactions every year.

The data flows in two directions. Information on non-UK users of UK RCASPs is sent to HMRC and then exchanged with foreign tax authorities in other CARF jurisdictions. Information on UK residents comes both from UK platforms and from overseas RCASPs in participating countries, giving HMRC a consolidated view of UK taxpayers’ crypto accounts and disposals.

What UK RCASPs must collect and report

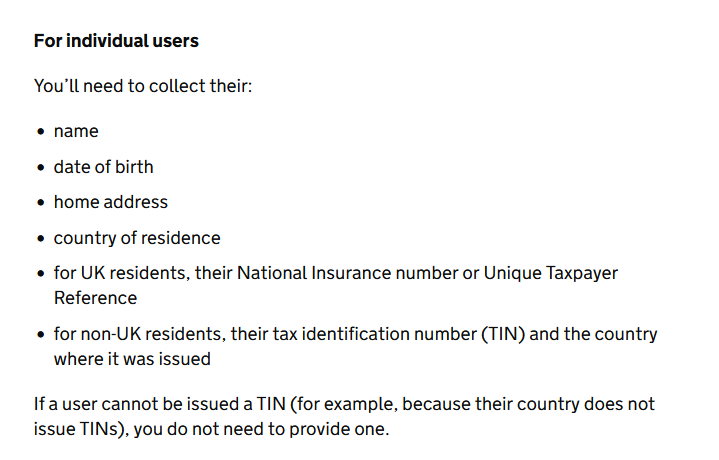

The core obligation for UK RCASPs is due diligence. Platforms must identify customers, obtain self-certified details such as name, address, date of birth, tax identification number and tax residency, and keep records that can support reporting and audits. False self-certifications can trigger penalties for users as well as for platforms that fail to challenge obvious errors.

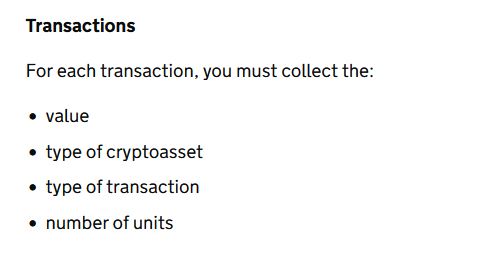

On the reporting side, CARF requires annual aggregated information on disposals and other relevant transactions: total proceeds, cost basis where available, the volume and type of crypto movements and, in some cases, counterparties. HMRC’s own policy note describes the measure as giving “visibility on the transactions of users of cryptoassets” so that it can risk-assess taxpayers and compare reported gains and income against third-party data.

The administrative burden is concentrated on a relatively small group (roughly 50 RCASPs are currently thought to be in scope) but it is not trivial. HMRC estimates one-off industry costs as negligible at the macro level, with ongoing administrative costs of around £0.8 million a year across the sector, and its own IT and compliance bill at about £69 million.

Timelines, enforcement and HMRC’s expected yield

CARF goes live in the UK on 1 January 2026. From that date, UK-nexus RCASPs must apply the new due diligence rules and begin collecting reportable data for the 2026 calendar year. The first full CARF reports will cover 2026 activity and are due in 2027, feeding into HMRC’s compliance work from the 2027–28 tax year onward.

The government expects CARF to raise meaningful but not transformative sums. Official estimates show an Exchequer impact of £40 million in 2026–27, £110 million in 2027–28, £85 million in 2028–29 and £80 million in 2029–30, with no significant macroeconomic effect forecast. Penalties for non-compliance include specific fines for failures to register, carry out due diligence or file accurate reports, with additional sanctions possible in cases of deliberate evasion.

Switzerland’s delay shows where CARF friction lies

The UK is moving early on CARF compared with some other financial centres. Switzerland has approved the OECD rules and will write CARF into domestic law from 1 January 2026, but has postponed the start of automatic crypto-asset information exchange until at least 2027 while it decides which partner countries to include and finalises technical implementation. First exchanges are currently expected in 2028 for 2027 data.

For HMRC, by contrast, the emphasis now is on onboarding RCASPs and building the data pipelines so that both cross-border and domestic crypto activity sit inside the same CARF-driven reporting grid from the first year of operation.

Disclaimer

This article is for information and education only. It is not investment, legal, tax or financial advice. Always do your own research and consider speaking to a qualified professional before making financial decisions.

More information

You can find detailed information about the Cryptoasset Reporting Framework:

- in the International Exchange of Information technical manual

- in the rules and commentary on the OECD’s website

You can also find out about international tax transparency standards on the OECD’s website.

If you have questions about the Cryptoasset Reporting Framework, you can email [email protected].

From the YFarmX archive · originally published on the previous site