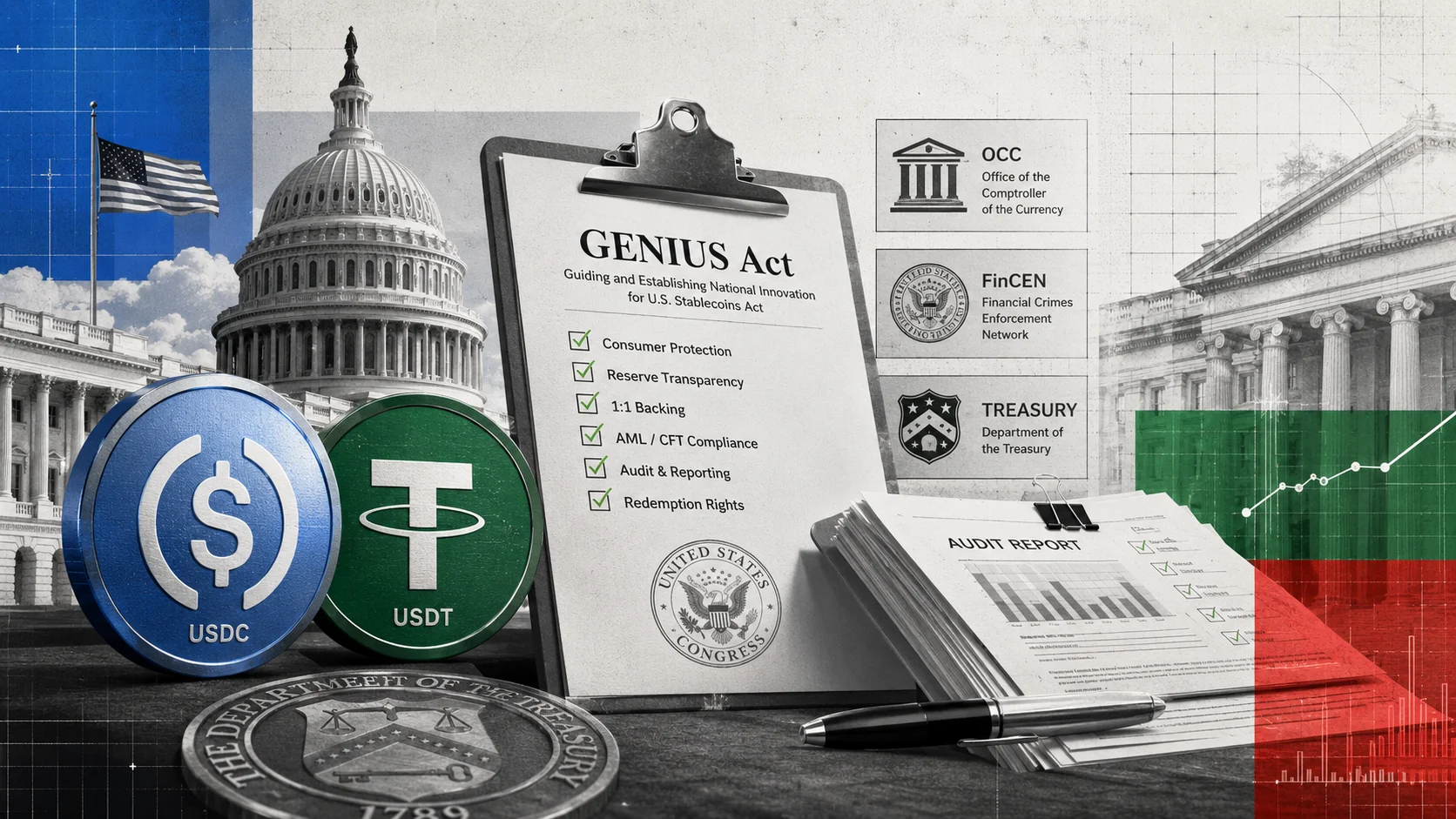

GENIUS Act stablecoin rules hit their deadline: the day digital dollars grew up

Today, 18 July 2026, is the statutory deadline for the GENIUS Act stablecoin rules, and Washington has spent the past month in an uncharacteristic sprint to meet it.

Today, 18 July 2026, is the statutory deadline for the GENIUS Act stablecoin rules, and Washington has spent the past month in an uncharacteristic sprint to meet it. One year after President Trump signed the Guiding and Establishing National Innovation for US Stablecoins Act into law, at least six federal agencies are due to finalise the regulations that will decide who may issue a digital dollar in the United States, and on what terms.

The line-up is formidable. The Office of the Comptroller of the Currency proposed its framework in March, followed in April by the Federal Deposit Insurance Corporation, the Treasury, the National Credit Union Administration, and a joint anti-money-laundering proposal from FinCEN and OFAC. Every major comment period closed by 9 June, leaving the agencies roughly five weeks to digest thousands of submissions and publish final text. The OCC’s proposal sets the tone: only permitted issuers may offer payment stablecoins in the US, and service providers may not sell tokens from anyone else.

The substance is less glamorous than the politics, which is rather the point. The GENIUS Act stablecoin rules require full one-to-one reserve backing in cash and short-dated instruments, redemption within two days, regular audits, and a proposed capital floor of five million dollars for issuers. FinCEN’s draft would treat permitted issuers as financial institutions under the Bank Secrecy Act, complete with customer due diligence, sanctions screening and, notably, the technical ability to freeze or block impermissible transactions. A programmable dollar, it turns out, comes with a programmable off switch.

Scale determines the supervisor. Issuers with under ten billion dollars outstanding may remain under state oversight; cross that line and a 360-day transition to federal supervision begins. Fixed compliance costs of this kind tend to be a rounding error for Tether and Circle and a serious problem for everyone else, which is why analysts have started describing the coming period as a consolidation phase rather than a land grab.

One widespread misreading deserves correcting. Today is the rulemaking deadline, not the day the law bites. The GENIUS Act takes effect on the earlier of 18 January 2027 or 120 days after the final regulations land, so issuers will have a compliance runway measured in months. What today does is start the clock, and clocks in financial regulation have a way of concentrating minds.

The stakes are considerable. The payment stablecoin market is worth somewhere between 230 and 325 billion dollars depending on what one counts, dominated by Tether’s USDT and Circle’s USDC, and increasingly courted by banks, card networks and fintechs building settlement rails on top of it. The law passed with genuine bipartisan force, 68 to 30 in the Senate and 308 to 122 in the House, a rarity for anything touching crypto.

For users, the immediate experience will change little. The framework targets issuers and intermediaries first; nobody’s wallet stops working on Monday. The pressure will surface downstream, in onboarding checks, redemption procedures and which tokens exchanges are still willing to list for American customers.

Whether every agency actually publishes on deadline day remains an open question, and a partial landing would be entirely in character for a six-agency co-ordination exercise. Either way, the GENIUS Act stablecoin rules mark the moment the digital dollar stopped being a regulatory grey area and became, for better or worse, paperwork. Full texts will appear via the Treasury, FinCEN and the OCC as they are finalised.

The sorting has already begun. Analysts describe the framework as dividing the market into regulatory winners and laggards: issuers with audited reserves, US entities and bank relationships stand to inherit the compliant volume, while offshore issuers face a choice between meeting the foreign-issuer conditions or watching American distribution channels close. Tether, whose reserves and domicile have drawn a decade of questions, has the most riding on how generously those conditions are drafted. The interest prohibition adds a further twist, pushing competition away from yield and toward integration, transparency and traceability, which suits the banks now circling the sector rather nicely.

Sources

- US Treasuryhome.treasury.gov

- FinCENfincen.gov

- OCCocc.gov

- OCCocc.gov