Solana ETF inflows defy a 57 per cent drawdown: every July session in the green

There is stubborn, and then there is the Solana ETF investor. Solana ETF inflows have stayed positive on every single trading day of July so far, a streak that would be unremarkable in a bull market and is borderline eccentric in this one.

There is stubborn, and then there is the Solana ETF investor. Solana ETF inflows have stayed positive on every single trading day of July so far, a streak that would be unremarkable in a bull market and is borderline eccentric in this one. The token has fallen roughly 57 per cent since the US spot products launched on 28 October 2025, trading in the high 70s against triple digits at listing, and the funds have absorbed money throughout. Cumulative net inflows have now passed one billion dollars, according to data tracked by SoSoValue.

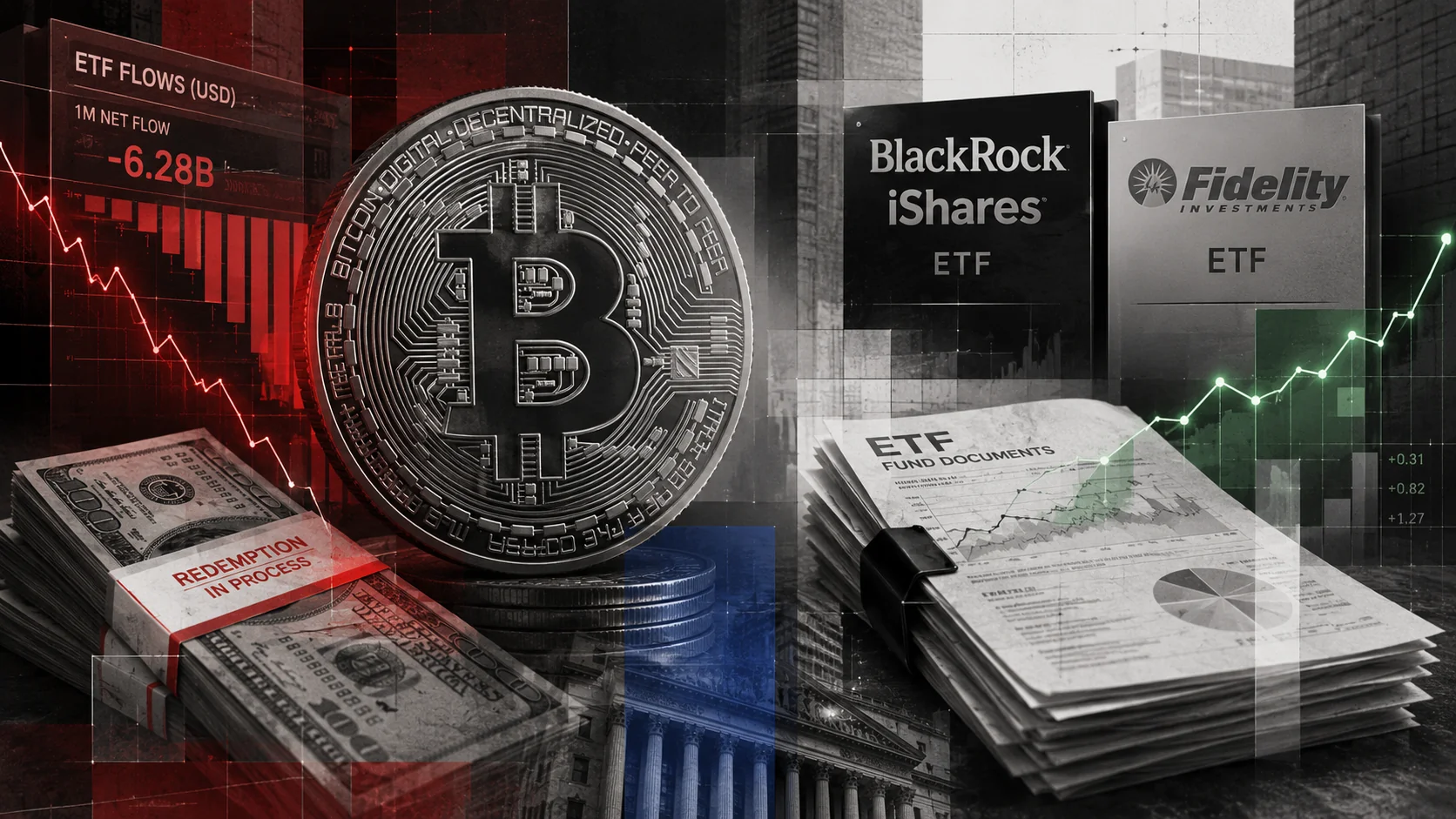

The recent numbers are modest in absolute terms and striking in context. The first full trading week of July produced 5.75 million dollars of net inflows across the four active products, 21Shares’ TSOL, Bitwise’s BSOL, Grayscale’s GSOL and Fidelity’s FSOL, per CoinGlass data. On 6 July alone, daily net inflows reached 103,020 SOL across the group. Set that against the bitcoin complex, where spot funds bled 527 million dollars the same week and extended a two-month outflow stretch, and the divergence looks less like noise and more like a preference.

What explains buyers averaging into a 57 per cent drawdown through a regulated wrapper? The uncharitable read is bag-holding with extra paperwork. The charitable one notes that Solana’s fundamentals have decoupled from its price: the network processed over a billion transactions in a single week this month, application revenue remains among the strongest in the industry, and the chain has become the default venue for the payments and consumer experiments that actually onboard normal users. Institutions allocating through ETFs tend to run longer clocks than perpetual futures traders, and the flow data suggests they are treating the drawdown as an entry rather than an omen.

The plumbing beneath the products is evolving too. In an 8-K filed with the SEC on 7 July, 21Shares disclosed that TSOL will switch its pricing benchmark from the CME CF Solana-Dollar Reference Rate to the FTSE Digital Assets Index, effective 24 August 2026, with the old licensing agreement ending a week later. For holders nothing changes about the fund’s objective or exposure; for the industry it is a small sign of maturity that benchmark providers are now competing for crypto index business the way they long have for equities. Issuer documentation is available from 21Shares, Bitwise, Grayscale and Fidelity, with filings at the SEC.

The risks have not gone anywhere. Solana ETF inflows measured in single-digit millions cannot offset macro pressure, and a market that rotates hard back into bitcoin, or simply out of risk, would test the streak quickly. The CLARITY Act’s fate adds a regulatory wildcard, since the bill would cement the commodity treatment underpinning these products.

Still, in a summer defined by record bitcoin fund redemptions, the most consistent bid in American crypto ETFs has been for the asset with the ugliest chart. Either the buyers know something, or they are about to provide an expensive lesson in the difference between conviction and stubbornness. The daily prints, for now, keep coming in green.

The first-year verdict on the product class is therefore stranger than anyone forecast at the October launch. These funds have never known a bull market, arriving days before the cycle top and spending their entire existence in drawdown, yet redemption pressure of the kind battering bitcoin funds has simply not appeared. Benchmark competition arriving this early, with FTSE displacing CF Benchmarks on TSOL, signals that index providers expect the category to persist and grow, since nobody fights over the pricing of a product they expect to close. Institutional infrastructure, once installed, has a habit of finding its own demand.